Yatharth Hospital & Trauma Care Services Ltd. is one of the leading healthcare service providers primarily in the Delhi NCR region. It was founded by Ajay Kumar Tyagi in the year 2008 with a vision to provide affordable and high-quality healthcare service. Since its inception, it has expanded its footprint, offering a wide range of specialty medical services.

Yatharth Noida Extension and Greater Noida Hospital are the 8th and 10th largest hospitals in Delhi NCR. The total bed capacity of all my 5 hospitals stands at 2100+ beds of which 455 are ICU beds. The company has completed 16,165 surgeries and 15,359 dialysis procedures in FY23.

Company Timeline with Key Achievements and Milestones

2008: Incorporation of the company by Ajay Kumar Tyagi and commencement of operation.

2010: Establishment of the 1st hospital in Greater Noida.

2013: Establishment of a 2nd hospital in Noida with 250 beds.

2018: Expansion of Greater Noida Hospital to 400 Beds

2019: Establishment of 3rd Hospital in Noida Extension.

2022: Adding 4th Hospital by acquiring Jhansi Orchha Hospital adding 305 beds.

2023: Got Listed on NSE and BSE

2024: Added 5th Hospital by acquiring Asian Fidelis Hospital adding 200 beds. Adding 6th and 7th Hospitals in their portfolio. Model Town, Delhi with 300 beds and Faridabad with 400 beds. Raised Rs. 6,250mn via QIP

Area of Clinical Specialties:

- Internal Medicine

- Nephrology & Urology

- Cardiology

- Neurosciences

- General Surgery

- Pulmonology

- Orthopaedics,

- Spine & Rheumatology

- Gynaecology

- Oncology

- Paediatrics

- Others

Geographical Presence:

Yatharth Hospital & Trauma Care Services Ltd. has a total of 5 hospitals and 2 upcoming Hospitals that will be operational by Q1FY26. 4 out of 5 are concentrated in the Delhi NCR region and 1 in Jhansi. The most recent acquisitions are the Asian Fidelis Hospital in Faridabad, rebranded as Yatharth Hospital, Faridabad, and Model Town Hospital, Delhi. The company plans to add 1 hospital each financial year from FY24 to FY26, primarily in North India.

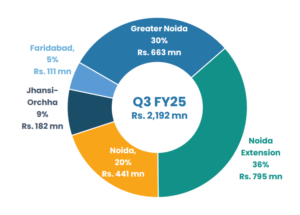

Revenue Bifurcation:

Noida Branch is the highest contributor to the revenue followed by Noida Extension and Greater Noida. Jhansi-Orchha branch which was acquired in 2022 has 305 beds capacity but has only 47% occupancy rate increase from 27% last year which is still quite low. The company has yet to report data on the Faridabad branch as it was acquired this year and operationalized on May 12.

Speciality wise:

- Oncology: 18%.

2. Internal Medicine: 12%.

3. Nephrology & Urology: 12%.

4. Cardiology: 11%.

5. Neurosciences: 8%.

6. General Surgery: 7%.

7. Gastroenterology: 7%.

8. Orthopedics, Spine & Rheumatology: 7%.

9. Gynecology: 5%.

10. Pulmonology: 5%.

11. Pediatrics: 3%.

12. Others: Remaining share